The client call I recently received sounded familiar. On the phone, a distraught business owner described what he had found: “I caught her writing checks to herself; one for $5,000! She has worked here for years and is the best employee we have.” I expressed my regrets about what he was experiencing and asked several clarifying questions. In all seriousness, he asked me, “Do you know her?”

No, I didn’t know the fraudster who took $550,000 from him, but I definitely know her type. The most heartbreaking part of my job is the realization that most fraud schemes are easily detectable. No matter the amount of loss or the type of scheme, there are common denominators that business owners can learn from.

Fraudsters are typically well-liked by owners/management.

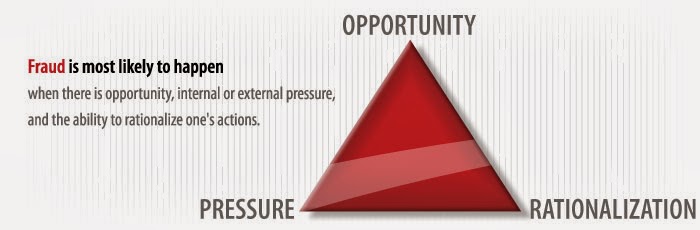

Would you give the keys to your kingdom (i.e. access to your money) to someone you didn’t like? Fraud occurs when someone is experiencing an internal pressure (e.g. debt, unemployed spouse, family crisis), can rationalize their behavior (“I am worth more.” “I will pay it back next time.”) and has opportunity to commit the act. This can occur when someone has access to the money and knows they are trusted in their job. Fraudsters are affable and have an answer to everything. They know you’ll believe them and they don’t have to show “proof” when you ask a question.

Ask questions and demand backup documentation, even if you know the answers. Employees are less likely to perpetrate a crime if they know there is oversight over their work. Trust is not an internal control.

Reviewing monthly bank statements and cancelled checks will uncover the majority of all frauds.

Well over 50 percent of all frauds are attributable to fraudulent disbursement schemes. Overpaid payroll, fictitious expense reimbursements, and check tampering schemes are so common that it’s often the first place I look.

Review your bank statement every month. Are there any electronic payments that look odd to you? Ensure your bank returns cancelled check images. Are there payments going to any individuals or vendors that are out of place? What about payments to credit cards, utilities or other common vendors used by businesses and individuals? Are there two per month, indicating that someone is paying your bills in addition to their own? This review should be performed by someone other than the person in charge of accounts payable.

Incoming cash and checks are easy to steal.

Incoming cash and checks are easy pickings for fraudsters who think they need your money. Yes, you read that correctly, incoming checks written to you are easily converted to benefit the fraudster – just ask my recent client who lost over $250,000 from a similar scheme!

Internal controls over cash receipts should include a receipt method for all monies received. Those receipts should be sequenced and reconciled to the amount of cash and checks deposited to the bank. Checks should be endorsed the moment received and all funds should be taken to the bank daily. Review your accounting records to ensure no unauthorized credits or write-offs have been posted to customer accounts, which would indicate money has been skimmed.

Most frauds exceed six figures and have occurred for 18 months by the time they are uncovered. Being a business owner myself, I know how busy you are. I also know how you love running your business and bookkeeping is a chore (yes, even this accountant thinks so!). Internal controls and proper oversight do not have to be cumbersome, involve multiple people, or cost more. Keep it simple and effective and save yourself the heartache of learning that your best employee has actually been your worst one.

This piece originally appeared as an Accounting & Finance column in the January 24, 2014 edition of the Vancouver Business Journal.